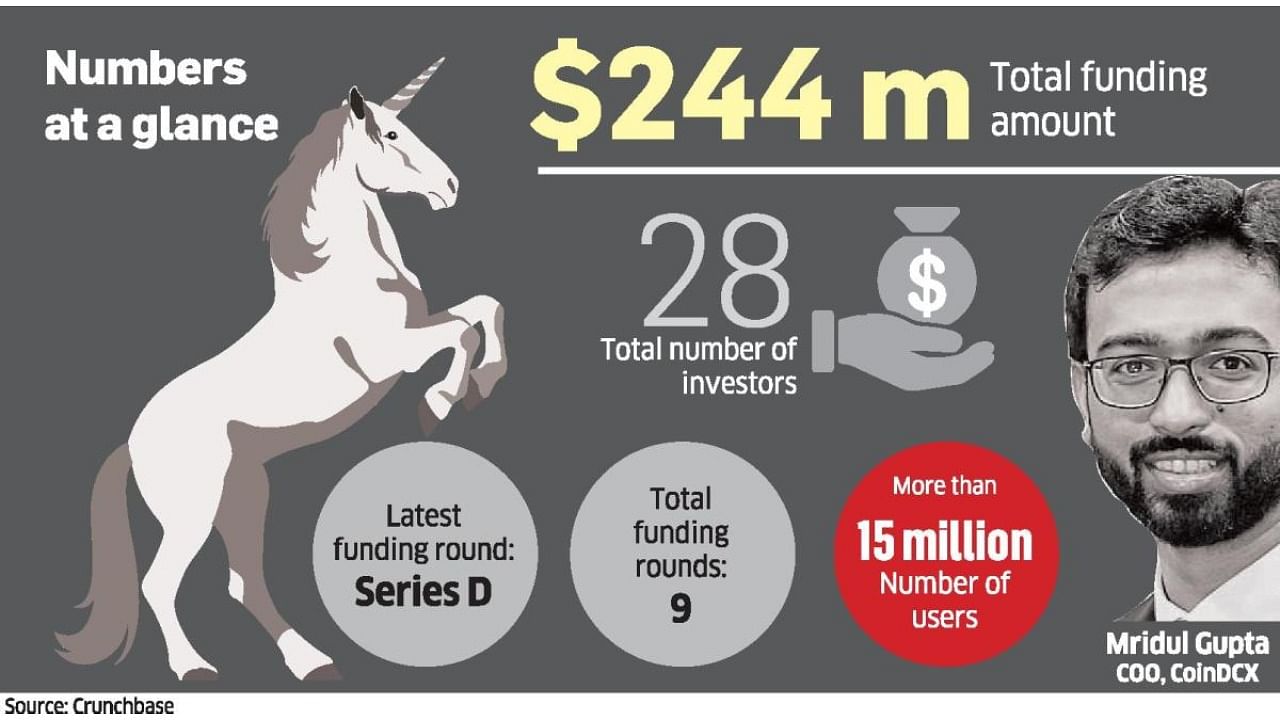

<p>For Mridul Gupta, the chief operating officer of India’s first crypto unicorn CoinDCX, “business as usual” has taken on a new meaning.</p>.<p>He joined the crypto exchange last year “to drive growth for CoinDCX business and build India’s leadership in a decentralised future”.</p>.<p>Fast forward to the summer of 2022, he and other members of the startup’s top management team are busy trying to convince Indian regulators and banks to work with crypto exchanges.</p>.<p>“Business as usual for me is different from what it means to you,” Gupta told <em><span class="italic">DH</span></em>, while sipping his coffee on a rainy evening in Bengaluru last week.</p>.<p>Like many crypto exchanges in India, CoinDCX – which according to Gupta has 15 million users– has seen a huge drop in trading volume after the government started taxing crypto assets from April 1. Additionally, regulatory uncertainty has made banks unwilling to allow crypto transactions through their networks.</p>.<p>To make things worse, the National Payments Corporation of India, which enables digital payments and settlement systems, recently expressed its reservations on the fund flows through the Unified Payments Interface (UPI) for crypto trades, putting a damper on the expansion plans of many crypto exchanges in India.</p>.<p>Gupta and his colleagues have seen trading volumes at CoinDCX drop by about 40 per cent since the UPI ban, forcing them to act quickly and work harder to convince the powers that be. “The topics of discussions have definitely intensified. Number of sittings with banks and regulators does not matter. We are more concerned about the outcome,” Gupta said. He is celebrating the small wins.</p>.<p>“To our advantage, questions of banks have changed from basic ones like what is crypto to how transactions happen,” Gupta told <span class="italic">DH</span>.</p>.<p>The worst might not be over for the crypto industry. </p>.<p>“We have to resolve this (UPI) issue and we will. I do not have a time as to when it will be resolved but the bigger problem is 1 per cent TDS on crypto from July 1. That will dent an investor’s pocket, which will, in turn, cause them to move to offline channels. That will bring down our volumes,” said Gupta. </p>.<p>While the government has started taxing all the gains from trading in cryptocurrencies and similar digital assets at a flat 30 per cent from April 1, another 1 per cent tax deducted at source (TDS) will be calculated when any such transaction takes place from July 1.</p>.<p>The TDS will affect the larger investors more and be less of a worry for small investors, pointed out Kumarmanglam Vijay, Partner at J. Sagar Associates.</p>.<p>“Clearly, TDS requirement has been brought in so that the government gets information on transactions in crypto. 1 per cent of the consideration is a small amount compared to the 30 per cent tax rate on gains derived from the transfer of crypto. Individuals who are not in any business or profession are exempt from withholding tax where the amount paid is less than Rs 50,000 during the financial year. Therefore, it is intended for reporting larger transactions to the government,” Vijay explained.</p>.<p>Despite the long list of issues plaguing the crypto industry in India, it still has more cryptocurrency holders than any other country in the world. It also features among the top five countries when it comes to the percentage of population that owns cryptocurrency. And that’s because of crypto owners like Samrat Mazumdar.</p>.<p>He switched to Binance to avoid the regulatory hassles faced by the Indian exchanges and the new taxes tied to crypto transactions in Asia’s third-largest economy.</p>.<p>“Now, with the tax regime, I do not think I will come back to using an Indian exchange. I am so glad I took the decision to move to using a foreign exchange. I will not return till tax slabs are rationalised in India,” Mazumdar said, confirming Gupta’s worst fears.</p>.<p>So will CoinDCX abandon India and go elsewhere?</p>.<p>“Payment gateways are down is the short-term threat. I cannot give a timeline as to when it will be resolved but the long-term opportunity is that regulations are being worked on. But you know, we will come back stronger once the payment gateway is sorted out mainly because markets are volatile and people would want to invest in crypto. For us, there is no question of what if it doesn’t happen. We have to somehow make it happen,” Gupta told <em><span class="italic">DH</span></em>.</p>.<p>CoinDCX plans to educate potential investors, work with regulators and introduce new products even amid larger uncertainties, he said.</p>.<p>“We already have a systematic investment plan product. We are working on various timelines for our SIP product. We want a lot of investors and not just traders,” Gupta said. CoinDCX is currently the most valued crypto exchange.</p>

<p>For Mridul Gupta, the chief operating officer of India’s first crypto unicorn CoinDCX, “business as usual” has taken on a new meaning.</p>.<p>He joined the crypto exchange last year “to drive growth for CoinDCX business and build India’s leadership in a decentralised future”.</p>.<p>Fast forward to the summer of 2022, he and other members of the startup’s top management team are busy trying to convince Indian regulators and banks to work with crypto exchanges.</p>.<p>“Business as usual for me is different from what it means to you,” Gupta told <em><span class="italic">DH</span></em>, while sipping his coffee on a rainy evening in Bengaluru last week.</p>.<p>Like many crypto exchanges in India, CoinDCX – which according to Gupta has 15 million users– has seen a huge drop in trading volume after the government started taxing crypto assets from April 1. Additionally, regulatory uncertainty has made banks unwilling to allow crypto transactions through their networks.</p>.<p>To make things worse, the National Payments Corporation of India, which enables digital payments and settlement systems, recently expressed its reservations on the fund flows through the Unified Payments Interface (UPI) for crypto trades, putting a damper on the expansion plans of many crypto exchanges in India.</p>.<p>Gupta and his colleagues have seen trading volumes at CoinDCX drop by about 40 per cent since the UPI ban, forcing them to act quickly and work harder to convince the powers that be. “The topics of discussions have definitely intensified. Number of sittings with banks and regulators does not matter. We are more concerned about the outcome,” Gupta said. He is celebrating the small wins.</p>.<p>“To our advantage, questions of banks have changed from basic ones like what is crypto to how transactions happen,” Gupta told <span class="italic">DH</span>.</p>.<p>The worst might not be over for the crypto industry. </p>.<p>“We have to resolve this (UPI) issue and we will. I do not have a time as to when it will be resolved but the bigger problem is 1 per cent TDS on crypto from July 1. That will dent an investor’s pocket, which will, in turn, cause them to move to offline channels. That will bring down our volumes,” said Gupta. </p>.<p>While the government has started taxing all the gains from trading in cryptocurrencies and similar digital assets at a flat 30 per cent from April 1, another 1 per cent tax deducted at source (TDS) will be calculated when any such transaction takes place from July 1.</p>.<p>The TDS will affect the larger investors more and be less of a worry for small investors, pointed out Kumarmanglam Vijay, Partner at J. Sagar Associates.</p>.<p>“Clearly, TDS requirement has been brought in so that the government gets information on transactions in crypto. 1 per cent of the consideration is a small amount compared to the 30 per cent tax rate on gains derived from the transfer of crypto. Individuals who are not in any business or profession are exempt from withholding tax where the amount paid is less than Rs 50,000 during the financial year. Therefore, it is intended for reporting larger transactions to the government,” Vijay explained.</p>.<p>Despite the long list of issues plaguing the crypto industry in India, it still has more cryptocurrency holders than any other country in the world. It also features among the top five countries when it comes to the percentage of population that owns cryptocurrency. And that’s because of crypto owners like Samrat Mazumdar.</p>.<p>He switched to Binance to avoid the regulatory hassles faced by the Indian exchanges and the new taxes tied to crypto transactions in Asia’s third-largest economy.</p>.<p>“Now, with the tax regime, I do not think I will come back to using an Indian exchange. I am so glad I took the decision to move to using a foreign exchange. I will not return till tax slabs are rationalised in India,” Mazumdar said, confirming Gupta’s worst fears.</p>.<p>So will CoinDCX abandon India and go elsewhere?</p>.<p>“Payment gateways are down is the short-term threat. I cannot give a timeline as to when it will be resolved but the long-term opportunity is that regulations are being worked on. But you know, we will come back stronger once the payment gateway is sorted out mainly because markets are volatile and people would want to invest in crypto. For us, there is no question of what if it doesn’t happen. We have to somehow make it happen,” Gupta told <em><span class="italic">DH</span></em>.</p>.<p>CoinDCX plans to educate potential investors, work with regulators and introduce new products even amid larger uncertainties, he said.</p>.<p>“We already have a systematic investment plan product. We are working on various timelines for our SIP product. We want a lot of investors and not just traders,” Gupta said. CoinDCX is currently the most valued crypto exchange.</p>