Italy’s Deputy Prime Minister Luigi Di Maio accused his compatriot Mario Draghi of “poisoning the atmosphere” after the European Central Bank president warned that the country’s borrowing costs would escalate unless the government pared back its spending plans.

Prime Minister Narendra Modi wants to keep India’s economy firing as he campaigns for re-election next year.

His administration has been pressing the central bank to hand over a part of its surplus reserves to help meet budget goals and ease restrictions on corporate lending by state banks.

Reserve Bank of India Governor Urjit Patel has other priorities: Flush out the pile of non-performing loans clogging the banking system, insulate the rupee from emerging-market jitters, and keep a lid on inflation.

Tensions, which had been simmering for months, exploded into public view in late October when one of Patel’s top lieutenants, Deputy Governor Viral Acharya, delivered a passionate defence of central bank autonomy at a lecture attended by all central bank deputy governors.

The speech appears to have been motivated by the Modi administration’s threat to invoke Section 7 of the Reserve Bank of India Act, 1934, a never-used provision that allows the government to dictate policy to the bank’s chief on matters of public interest. Since then the nation’s newspapers have chronicled each twist and turn of the controversy, including going so far as speculating that Patel will quit in protest.

No respect

“Governments that do not respect central bank independence will sooner or later incur the wrath of financial markets, ignite economic fire, and come to rue the day they undermined an important regulatory institution,” Acharya told the gathering.

He pointed to the Argentine government’s intrusion into its central bank’s affairs in 2010, which spooked investors and triggered a surge in bond yields, with damaging consequences for the economy.

Acharya could have just as easily cited the experience of Turkey, where President Recep Tayyip Erdogan’s public attacks on the central bank’s independence caused the Turkish lira to plummet.

Like those countries, India relies on overseas money to fund investment and is vulnerable to a sudden reversal in sentiment.The rupee lost more than 10% of its value against the dollar this year, partly on concerns that a slow-moving crisis in the non-bank financial sector will dent growth.

While flagging risks to investment activity from tight money conditions, the central bank last month retained its 7.4% gross domestic product growth projection for the financial year ending March.

Truce signs

“These are not good times to be labeled a country which doesn’t respect the central bank’s autonomy,” Raghuram Rajan, a former RBI governor, said in a recent interview on local television.

“Running over a central bank has not been good for any economy.” Signs of a truce appeared recently, when a marathon nine-hour board meeting ended with the central bank agreeing to study the government’s demands, including a plan for sharing a part of its surplus capital.

While that’s a near-term relief for investors, it also suggests the tough decisions have been kicked down the road and could easily resurface again next year -- especially since

the government has proposed rules that will allow it greater supervision over the central bank.

Squabbles between the Reserve Bank of India and the government are nothing new. Rajan, a former International Monetary Fund chief economist, stepped down as bank governor in 2016 after a single term to return to a teaching post at the University of Chicago, having faced criticism from a prominent Modi ally who accused him of keeping rates too high and of not being “fully Indian” in his mindset.

Politicians piqued

In a memoir, his predecessor, Duvvuri Subbarao, recalled repeated run-ins with government ministers who “were piqued by the Reserve Bank’s tight interest rate policy on the ground that high interest rates were inhibiting investment and hurting growth” during his tenure, which lasted from 2008 to 2013.

Patel, who earned his PhD in economics from Yale University, was initially seen as being supportive of Modi’s policies, including the controversial decision to invalidate 86% of currency notes in circulation in late 2016.

Signs of strain began to emerge last year when Arvind Subramanian, Modi’s chief economic adviser at the time, accused the RBI of large and systematic errors in its forecasting methods that were causing it to overstate inflation.

The RBI has raised interest rates twice this year to tamp down inflation, which hit a 13-month low of 3.3% in October.

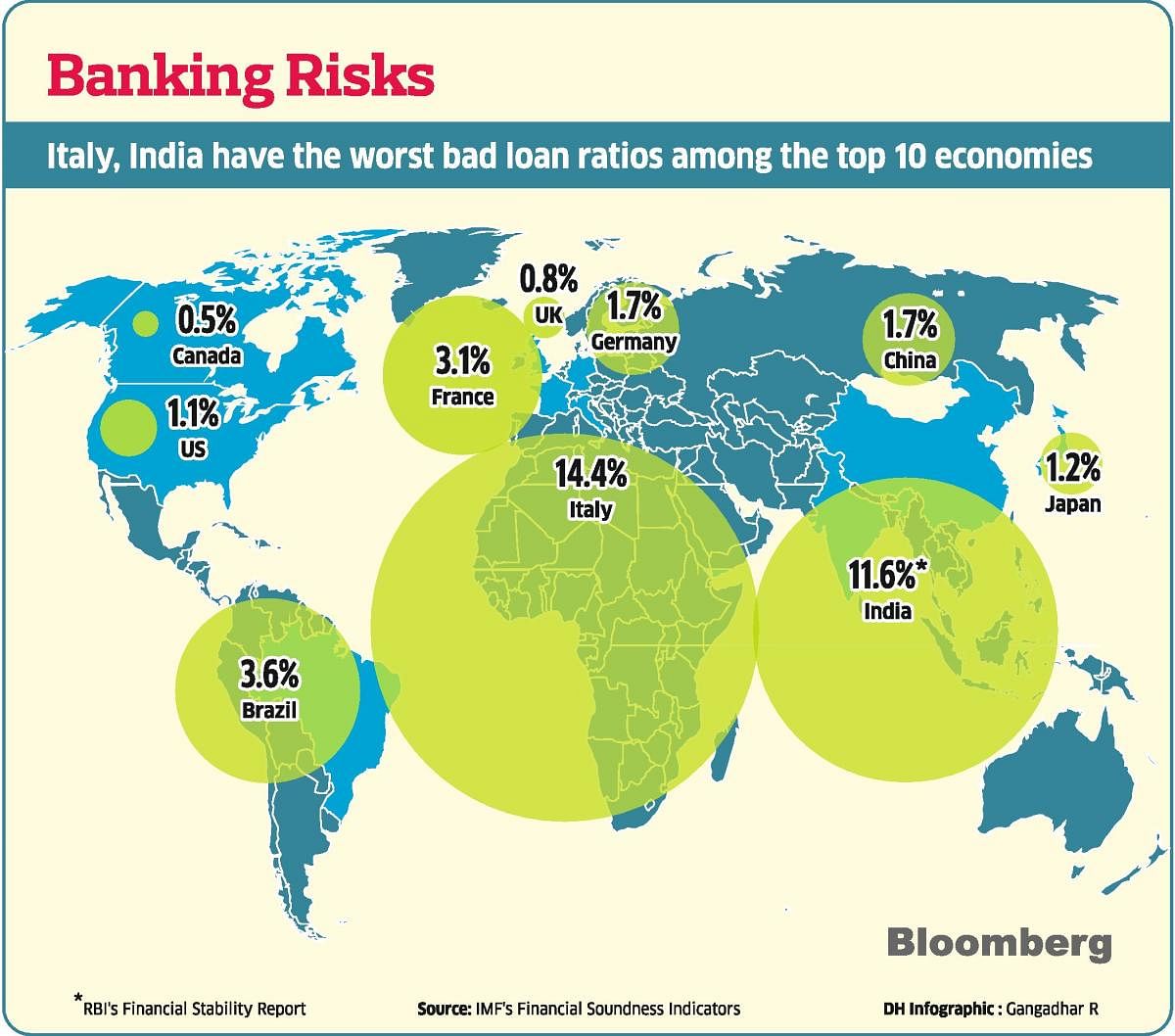

Another bone of contention has been Patel’s push to clean up the banking sector, which has one of the world’s highest levels of bad loans. That’s riled some in the political leadership who want loan delinquency rules eased for companies and tough new lending strictures on under capitalised state-run banks removed to boost economic growth before national elections in May.

Troubled investors

A bigger worry for investors has been the administration’s attempts to tap a portion of the central bank’s surplus reserves to compensate for a shortfall in revenue, which has been trailing targets despite the introduction last year of a national sales tax.

“There is a fear that the RBI’s reserves may be used to finance the fiscal deficit,” says Amartya Lahiri, director at the Centre for Advanced Financial Research and Learning, a Mumbai-based think tank, and a professor at the University of British Columbia.

“Markets may get spooked if that happens, since it will give the impression of fiscal dominance of the RBI by the government.”

(Disclaimer: This article first appeared on bloomberg.com/asia, and is published by special arrangement)