India will scrap its infamous retrospective tax of 2012 that made any capital gains resulting from the transfer of shares from a foreign entity, whose assets were located in India, taxable from 1962.

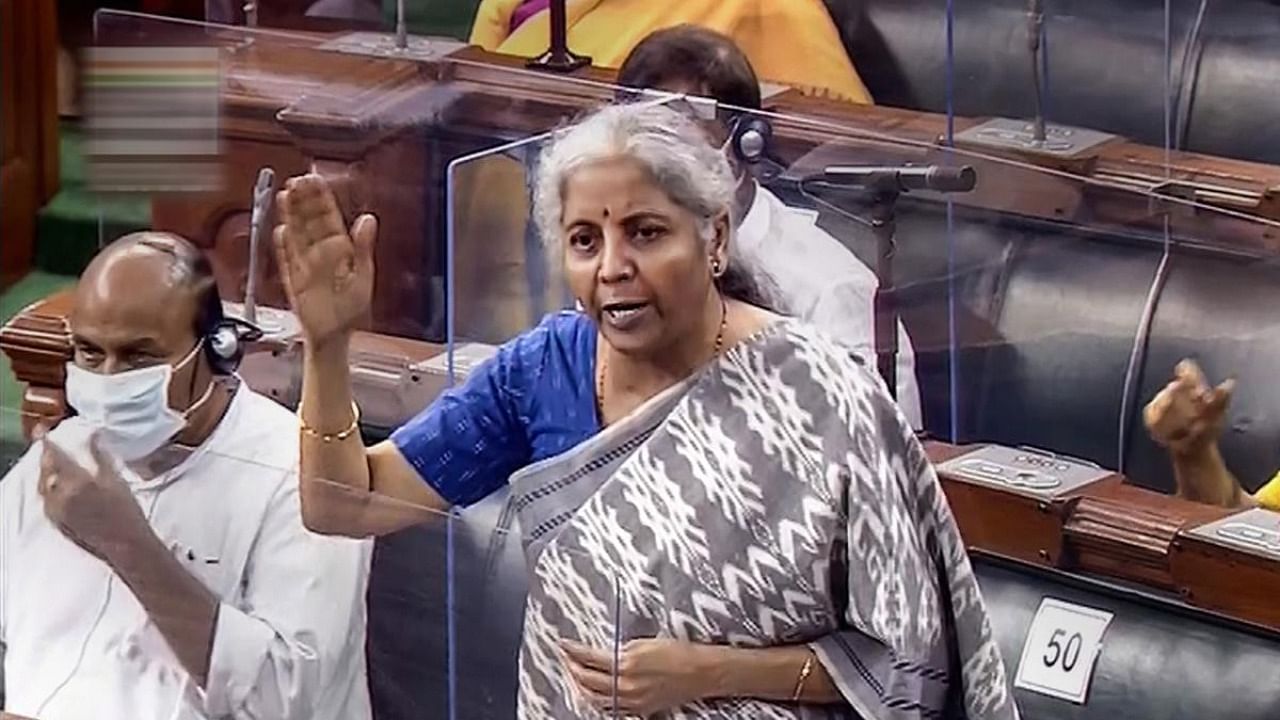

Finance Minister Nirmala Sitharaman on Thursday introduced a bill in the Lok Sabha that proposes to amend the Income Tax Act of 1961 so as to provide that no tax demand shall be raised in future on the basis of the said retrospective amendment for any indirect transfer of Indian assets if the transaction was undertaken before May 28, 2012.

The bill also proposes to refund the amount paid in these cases without any interest.

The bill impacts retrospective tax cases of two big companies -- Cairn Energy Plc and Vodafone Group of the UK, both of which won international arbitrations against levy of retrospective taxes. Subsequently, Cairn sought to recover $1.2 billion from India.

The finance ministry said, "The issue of taxability of gains arising from the transfer of assets located in India through the transfer of the shares of a foreign company (hereinafter referred to as 'indirect transfer of Indian assets') was a subject matter of protracted litigation. Finally, the Supreme Court in 2012 had given a verdict that gains arising from indirect transfer of Indian assets are not taxable under the extant provisions of the Act."

But the then finance minister Pranab Mukherjee circumvented the ruling by proposing an amendment to the Finance Act of 2012, which gave the I-T Department power to retrospectively tax such deals. The Act was passed by Parliament that year, and the onus of paying the tax fell back on Vodafone.

The Supreme Court ruled that Vodafone Group’s interpretation of the Income-Tax Act of 1961 was correct and that it did not have to pay any taxes on the stake purchase.