Blockchain is the future — just like Virtual Reality, Internet of Things, 3D Printing and Big Data were at one point. In India, proponents of Blockchain suggest using it to solve, among other things, the problems of land titles, agrarian rights, and financial exclusion. Smart contracts, especially, promise to replace the existing, cumbersome legal system and replace it with lines of code that are guaranteed to be objective and neutral. This utopian idea of a world that is run on a trust-less, objective, immutable system that is open, free and fair is one that is easy and tempting to buy into. Unfortunately, it is an ideal that does not stand up to close scrutiny.

Digital contracts have existed for several decades — insurance premiums being deducted automatically from bank accounts and the ordering books on Amazon are common examples. These, however, are considered to be ‘weak’ contracts, which means that they can be revoked or modified later. The main benefits of using ‘strong’ smart contracts are that they are self-enforcing and objective. The contract is represented by a series of computing instructions and the code, they say, being mathematically, logically and semantically precise, supposedly does not need to be further interpreted by the slow, cumbersome legal machinery.

Some suggest integrating the smart contract with the traditional court system. This would actually be completely antithetical to the idea of Blockchain. The massive resources consumed by the Blockchain network is solely to ensure its immutability, irreversibility and guaranteed execution. Allowing a court to repudiate smart contracts would be against these fundamental principles and there would be virtually no difference between a traditional digital contract and a Blockchain smart contract, except that the latter would require far more resources to maintain.

One of the most important aspects in the formation of a contract is the ‘intention’ of the parties. Ambiguity in its terms is resolved by referring to the context during formation so as to not unfairly prejudice any party, and agreements that are too uncertain are treated as void. In a smart contract, however, this basic tenet is thrown out of the window and the wording of the contract, however impractical, undesirable, or illegal, will be followed to the dot. Later changes, like an outbreak of war, which would normally frustrate traditional contracts, would not alter the execution of a smart contract.

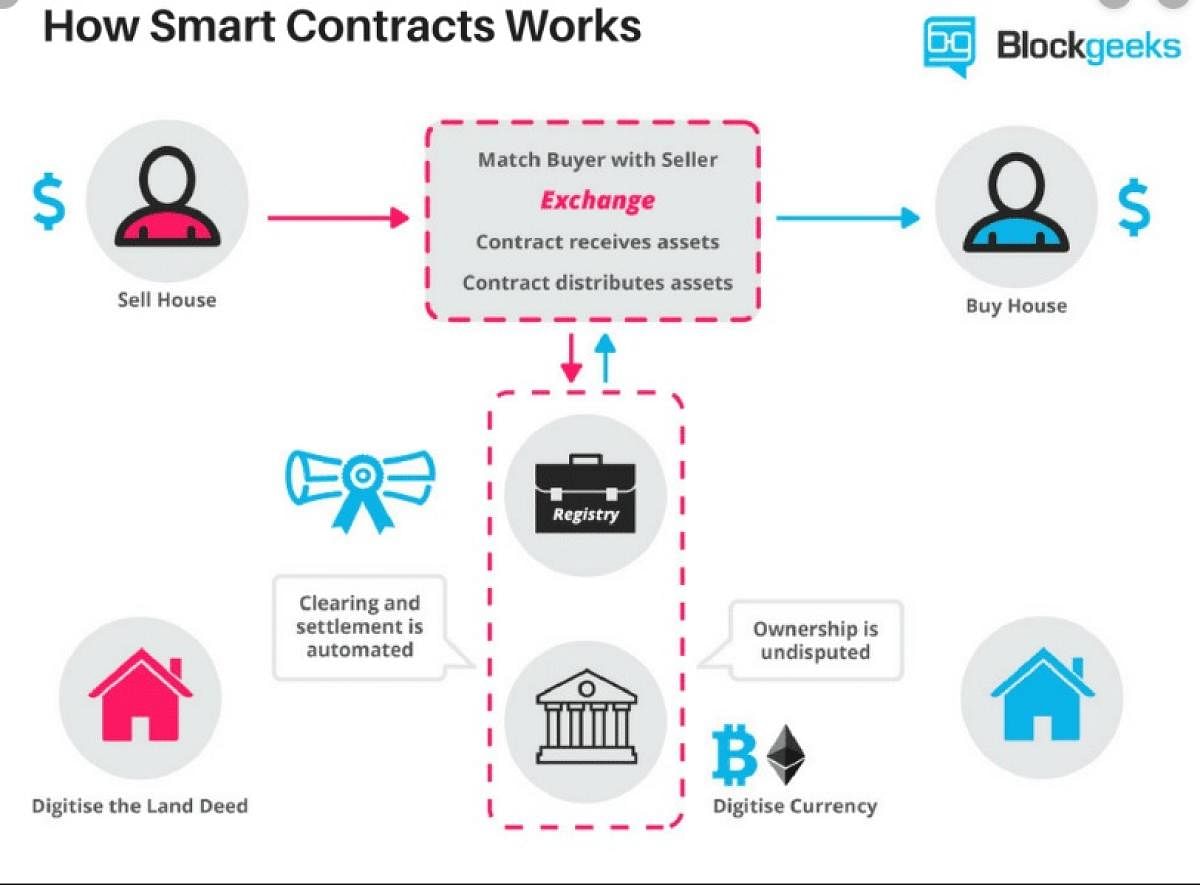

Most contracts entered into will have to interact with the physical world — delivery of goods, construction of a house, etc. A smart contract residing in the digital space will thus need some means to communicate with the real world to ascertain whether certain conditions have been fulfilled. This is the job of the ‘oracle’.

An ‘oracle’ in Blockchain is a mutually trusted third party, which may be a program itself, that feeds information into the smart contract. At some point along a supply chain, however, these oracles will have to be fed information by humans typing data into a computer. For all the promised immutability, trustlessness, and security of the Blockchain, it will still be subject to human error. Matt Levine of Bloomberg captured this perfectly — ‘My immutable unforgeable cryptographically-secure Blockchain record proving that I have 10,000 pounds of aluminium in a warehouse is not much use to a bank if I then smuggle the aluminium out of the warehouse through the back door.’ The oracle would have no way to assess subjective matters. Terms such as ‘satisfactory’ and ‘pretty’ are inherently subjective in nature and cannot be codified.

A much-touted use case for smart contracts is in the insurance sector, where timely payouts and disposal of claims will supposedly be guaranteed. Insurance companies spend massive amounts of money to investigate and assess claims. Claim assessments demand physical inspections, perusal of documents and interviews, and is a complex, time-consuming process that involves a lot of subjectivity. The claim that a few lines of code can reliably replace all this without massively increasing the cost of premiums for all other customers is ludicrous.

Intermediaries are caricatured by proponents of the Blockchain as greedy, dollar-eyed capitalists who trample on the poor. In doing so, they completely ignore the services and benefits provided by them — credit card companies also provide fraud protection; stock exchanges and brokers provide liquidity and leverage; lawyers ensure that the terms of a contract do not unfairly prejudice the rights of any one party; and banks provide loans on demand, foreign exchange, investments and more. The modern machinery of commerce depends on these crucial intermediaries for its efficient functioning.

For all the philosophical waxing about trust and security, the smart contract’s reliance on oracles reveals how there is still a need for neutral, trusted, third parties in most day-to-day transactions. Trustlessness being one of the major claims of Blockchain becomes quite weak when crucial elements of the smart contract rely on trust. The pressures of convenience and usability would inevitably lead to the centralization of oracles. This process will culminate in the proliferation of monolithic, centralized providers which provide oracles, contracts, and other services — a situation no different from today.

In a country like India that is fraught with illiteracy, the poor will continue to be exploited; the only difference being that the exploiter changes from regulated institutions to a faceless decentralized system lacking accountability. The poor will remain poor, while a different set, under the guise of openness, security, and inclusivity, replaces the old guard. The present legal system may not be perfect, but the system proposed to replace it is arguably worse. The Blockchain may be touted as a solution, but under the glamour and lights, it is nothing more than old ideas packaged in a new box.

(The writer is a student at NLSIU, Bengaluru)